When a severe storm strikes, property owners face two immediate challenges — the physical damage itself and the complex administrative process that follows. Although it can be challenging, understanding how insurance claims work for storm-damaged properties could help you protect your financial interests during the recovery phase.

Storm damage continues to escalate across the United States, in terms of both frequency and economic impact. In 2025, severe storms caused $52.3 billion in insured losses. The previous year saw 1,796 confirmed tornadoes, the second-highest number on record. This guide from Performance Adjusting Public Insurance Adjusters explains how to navigate the multistage claims process successfully, so you can prepare in case Mother Nature hits your home.

Key Takeaways

- Understand your coverage and act promptly: Familiarize yourself with your policy’s inclusions and exclusions. Then, immediately prioritize safety, document all damage, prevent further issues and report the claim after a storm.

- Navigate the claims process methodically: The insurance claims process involves a structured timeline and adjuster assessments. Be prepared for multiple payments and diligently maintain records of all interactions and expenses.

- Advocate for fair settlement: If the initial settlement is insufficient, consider obtaining independent estimates, hiring a public adjuster, or using the policy’s appraisal clause to dispute the offer and ensure proper restoration.

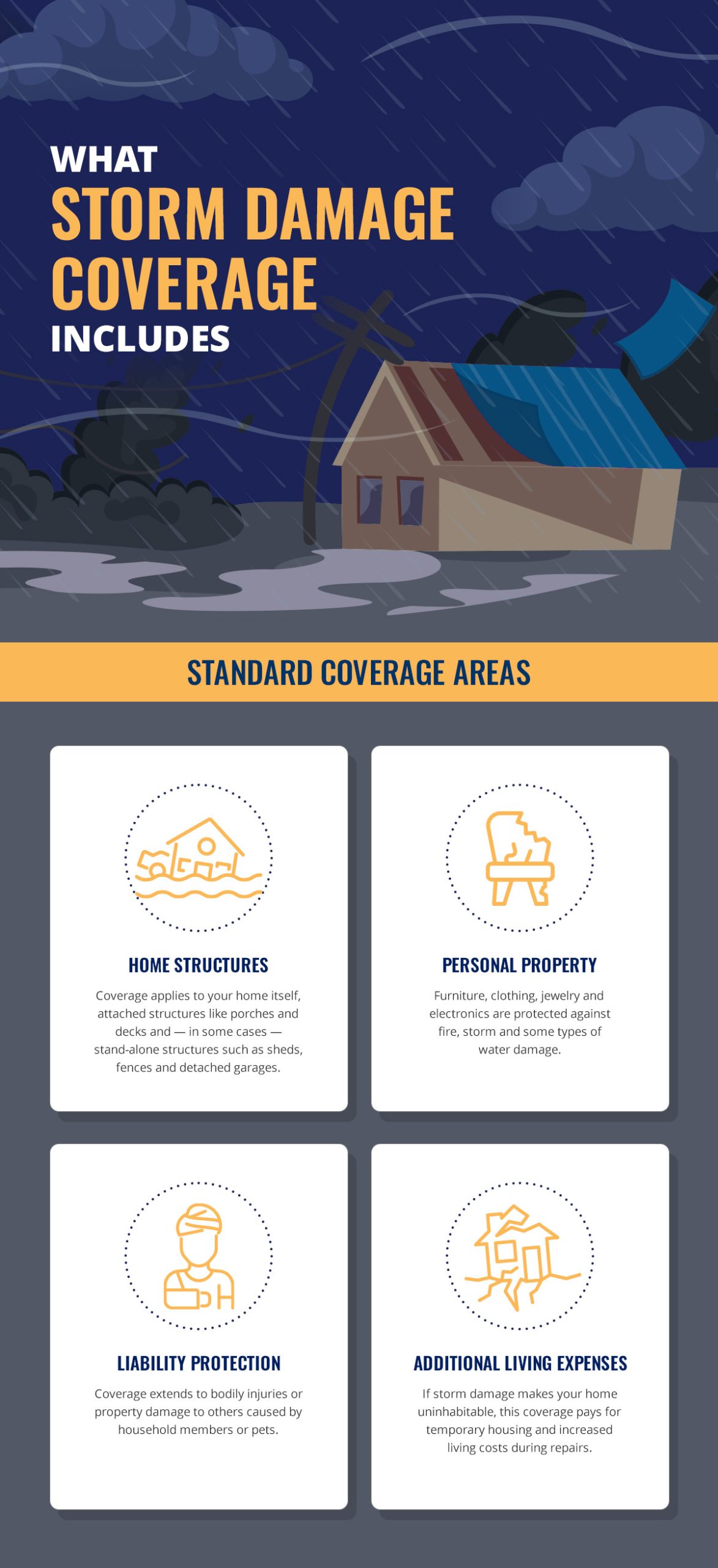

What Storm Damage Coverage Includes

Most standard homeowner’s insurance policies include wind and hail coverage, though you must often meet certain deductibles before coverage activates. Understanding what your policy protects helps you prepare for potential out-of-pocket costs and identify any coverage gaps.

Standard Coverage Areas

Standard homeowner’s insurance typically protects four main categories:

- Home structures: Coverage applies to your home itself, attached structures like porches and decks and — in some cases — stand-alone structures such as sheds, fences and detached garages.

- Personal property: Furniture, clothing, jewelry and electronics are protected against fire, storm and some types of water damage.

- Liability protection: Coverage extends to bodily injuries or property damage to others caused by household members or pets.

- Additional living expenses: If storm damage makes your home uninhabitable, this coverage pays for temporary housing and increased living costs during repairs.

Property owners can learn more about determining if property damage is covered.

What Standard Policies Don’t Cover

While standard homeowner’s insurance protects against many storm-related perils, critical gaps exist, and property owners should understand them before damage occurs.

Flood Damage

Damage from rising water requires separate flood insurance, which is available through two main options — the National Flood Insurance Program (NFIP) and private flood insurance. Property owners should evaluate both options based on their coverage needs, budget and flood risk zone.

Here are some key points on the NFIP:

- Coverage caps at $250,000 for home structure

- Coverage caps at $100,000 for contents

- Limited coverage for basement items

For private flood insurance, expect the following:

- Higher coverage limits than NFIP

- Faster or no waiting periods

- Can include additional benefits, like loss of use coverage

- Can be more expensive in high-risk flood zones

Property owners can benefit from understanding what type of water damage is covered by homeowner’s insurance to identify protection gaps.

Cosmetic Damage

An increasingly common provision affects how storm claims are evaluated — the cosmetic damage exclusion. This clause defines cosmetic damage as harm that affects appearance without impairing function, and these exclusions have become more prevalent in hail-prone regions.

The controversy centers on long-term implications. For example:

- Hail dents that don’t cause immediate leaks may still reduce your property’s structural lifespan.

- Seemingly minor damage can create future vulnerabilities.

- Property owners may face out-of-pocket costs for repairs to prevent long-term deterioration.

Immediate Steps to Take Following Storm Damage

The actions property owners take immediately after a storm can significantly impact their claim outcomes. There are four critical things you must do after storm damage to protect yourself, your property and your insurance claim.

Ensure Immediate Safety

Before you consider the next steps, ensure you and any other present individuals are safe by:

- Checking for injuries.

- Avoiding hazards.

- Contacting emergency services if necessary.

- Proceeding to the next steps with caution.

Document Everything

Before any cleanup begins, you need to document the storm damage thoroughly. Property owners should photograph and video all damage from multiple angles to create a complete record of storm impact.

Effective documentation should capture:

- Structural damage.

- Wide shots showing the damage in context.

- Close-ups of specific problems.

- Fallen debris.

- Water intrusion.

- General property condition immediately after the storm.

Modern smartphones automatically time-stamp images, which helps establish when damage occurred. If you do not have time-stamped images, ensure you make notes of the exact date and time of the damage. Generally, the more detailed your documentation, the more accurate your claim settlement will be.

Prevent Further Damage

Insurance policies require policyholders to take reasonable steps to prevent additional damage after a loss occurs. Common mitigation steps include placing tarps over roof holes, boarding up broken windows, removing standing water and making other reasonable temporary repairs.

Property owners should keep all receipts for emergency repairs, as these costs are typically reimbursable, depending on your coverage. However, you should generally wait for permanent repairs until an adjuster inspects your property. An adjuster can help you understand the storm damage claim process before proceeding with major restoration work.

Report the Claim Promptly

Most insurance policies include specific filing deadlines. Contact your insurer as soon as possible after discovering damage to start the official claims process.

When filing a claim, have your policy number, current contact details, home inventory (if available) and a basic description of visible damage ready. Most insurance companies offer multiple reporting methods, including 24/7 phone hotlines, mobile apps and online portals.

If you are uncertain about your coverage details, you can use this opportunity to ask your provider questions. For example, if your home is uninhabitable following the storm, you can request information on available additional living expenses.

The Claims Process Timeline

Storm damage insurance claims follow a structured timeline. Understanding this process helps property owners set realistic expectations and avoid potential delays.

State-Mandated Requirements

Most states have enacted statutory deadlines governing how quickly insurers must respond to claims. Time frames typically include:

- Claim acknowledgment: When the insurer confirms receipt of your claim.

- Investigation and coverage determination: When the insurer evaluates the damage caused by the storm.

- Payment or denial: When the insurer issues the settlement.

Different states have different mandatory deadlines. Contact your state insurance department’s consumer assistance office for specific deadlines that apply in their jurisdiction.

Realistic Time Frames

The actual duration depends heavily on the complexity and severity of your property damage. Simple property claims with minor damage can typically be resolved within weeks. Complex commercial claims, on the other hand, can extend to months, especially when business interruption coverage or multiple structures are involved. Large-loss claims with extensive damage may take many months or even years to reach the final settlement stage.

After catastrophic events affecting entire regions, insurers often deploy disaster response teams. However, the sheer number of simultaneous claims can still create delays beyond normal timelines. Ultimately, there is no way to determine exactly how long the claims process will take. Recent research suggests that, on average, homeowners will receive their final payment 40.7 days after making a claim.

What Happens After Filing

Once you file a claim, the insurer assigns a claims adjuster to assess your home’s damage. The adjuster schedules an inspection to view the property damage in person, evaluates both structural damage and personal property losses, and provides documentation to help determine the ultimate settlement amount.

You should attend all property inspections to point out all damage, including nonobvious issues.

Settlement Payment Structures

Insurance settlements for storm damage often arrive in multiple payments rather than in one check. The typical payment structure includes an emergency advance for immediate needs, a primary settlement after inspection and additional payments as repairs progress.

If a mortgage exists on your property, the settlement structure becomes more complex. Structural damage payments may be made payable to both the property owner and the lender. Lenders often place these funds in escrow accounts, releasing money as work is completed.

Understanding Adjusters

The term “adjuster” covers distinct roles with different loyalties. Insurance companies assign adjusters to handle claims on their behalf, and these professionals may be direct employees or contracted specialists.

Company adjusters investigate losses and verify coverage, document damage through photographs and written reports, recommend payment amounts and use standardized estimating software. During inspections, storm damage claim adjusters photograph damage from multiple angles, take measurements, review contractor estimates and determine if the damage aligns with your policy’s coverage.

When Property Owners Disagree With Settlements

Initial settlement offers sometimes fall short of the actual cost to fully restore storm-damaged property. Several options exist for property owners who believe their settlement doesn’t adequately cover their losses.

Obtaining Independent Estimates

Hiring contractors for independent estimates provides a second opinion on restoration costs. Professional contractors may identify damage that the insurance adjuster overlooked or provide different repair methodologies that more accurately reflect quality restoration standards.

When independent estimates significantly exceed the insurer’s assessment, you can submit this documentation with detailed explanations. Insurers may reinspect your property, adjust their estimates or explain why they believe their original assessment remains accurate.

The Role of Public Adjusters

Public adjusters are licensed professionals hired by policyholders, not insurance companies. Unlike company adjusters who work for insurers, public adjusters exclusively represent the property owner’s interests.

Their services encompass comprehensive damage assessment, policy language review for applicable coverage, comprehensive documentation preparation and direct negotiation with insurance companies using their expertise. Public adjusters typically charge a percentage of the final settlement, with fees varying by state regulations and claim complexity.

The Appraisal Process

Most insurance policies include an appraisal clause that provides a structured dispute resolution mechanism. This process offers a middle ground between informal negotiation and formal litigation.

Each party selects an appraiser with relevant expertise, and these two appraisers jointly select an umpire who resolves disagreements. The process addresses the amount of loss but not coverage questions, moves faster than litigation, and requires each party to pay their own appraiser while splitting the umpire’s fee.

Maintaining Records

Throughout the claims process, property owners should document every interaction. This involves documenting:

- All correspondence with the insurance company.

- The date and name of every person contacted.

- Detailed notes about what was discussed.

- Time spent on claim-related activities.

- Receipts for all expenses incurred.

Common Complications

Several issues frequently complicate storm damage claims and require additional attention.

Secondary and Hidden Damage

Storms often cause cascading effects that aren’t immediately apparent. For example, if your roof is damaged by a storm, it might allow water intrusion, which can saturate insulation, damage interior finishes and create conditions conducive to mold growth.

Professional inspectors can help you identify issues not visible to you or insurance adjusters. Thorough initial documentation can reduce disputes about whether later-discovered problems resulted from the original storm or from an unrelated cause.

Preexisting Damage Disputes

Insurance companies routinely investigate whether damage existed before the storm event. Policies generally only cover new damage from insured events, not preexisting problems or deferred maintenance.

Maintenance records showing regular upkeep, periodic photographs of your property’s condition, and documentation showing its baseline condition before storms occur can become invaluable when insurers question whether damage resulted from the weather event or from prior conditions.

Business Interruption Claims

Commercial property owners with business interruption coverage can claim lost income when storm damage forces temporary closure. These claims require detailed financial documentation proving normal income levels and demonstrating losses directly attributable to covered damage.

Business interruption claims typically take longer to resolve because of extensive documentation requirements including accounting analysis, historical financial data, and calculations of lost business opportunities. Since insurers tend to be reluctant to cover hypothetical losses, negotiating business interruption claims can be complex, and you may require the assistance of a public adjuster.

Navigating Disputes

When questions arise, it’s important to communicate with your insurance provider effectively. To successfully navigate claims disputes, you should:

- Address queries directly with your insurer through documented communication.

- Request specific policy language that supports the insurance company’s decisions.

- Contact your state insurance department for consumer assistance if responses seem inadequate.

- Document all attempts to resolve concerns.

Managed Repair Programs and Contractor Selection

Some insurance policies include provisions directing policyholders to specific contractors or managed repair programs. Understanding these provisions helps property owners make informed decisions.

Understanding Managed Repair Programs

Under managed repair programs, insurers direct policyholders to contractors who have negotiated arrangements with the insurance company. The potential advantages of managed repair programs include:

- Faster contractor assignment.

- Streamlined communication between the insurer and contractor.

- Possible warranty programs backed by the insurer.

Potential disadvantages include:

- Loss of contractor choice.

- Potential delays during high-volume periods.

- Less control over repair quality and timeline.

Most states protect property owners’ right to choose their own contractors regardless of policy language.

Selecting Contractors

Choosing your own contractors gives you more control over your property repairs. Unlike managed repair programs, selecting independent contractors enables you to make a decision based on contractors’ expertise and reputation. Collaborating with independent contractors also gives you more direct control over the quality and timeline of repairs.

However, if you opt to choose your own contractors, there are certain pitfalls to avoid. When choosing contractors, you should:

- Obtain estimates from multiple contractors.

- Verify their licenses and insurance.

- Check references and reviews from past clients.

- Compare approaches and pricing across bids.

Warning signs to avoid include:

- Promises to handle your insurance claims without a clear explanation.

- Requests for assignment of claim proceeds.

- Pressure to sign contracts immediately.

- No verifiable business address or credentials.

Navigating Storm Damage Claims Successfully

Successfully navigating storm damage claims can be challenging and requires prompt action, thorough documentation and a clear understanding of the process.

From immediate steps to long-term documentation, property owners must remain on top of correspondence and actions throughout the claims process if they want to see fair settlement outcomes. While it’s impossible to fully predict and prevent storm damage to your property, understanding how insurance claims work for storm-damaged properties empowers you to protect your interests during what is often a stressful time.

While the process involves multiple stages, various parties and strict timelines, property owners who approach claims methodically can achieve positive outcomes and faster recovery times.